If you don't design for the wealth transfer, you will lose the relationship

What happens to a deposit when the account holder dies? And why is that question still treated as an edge case?

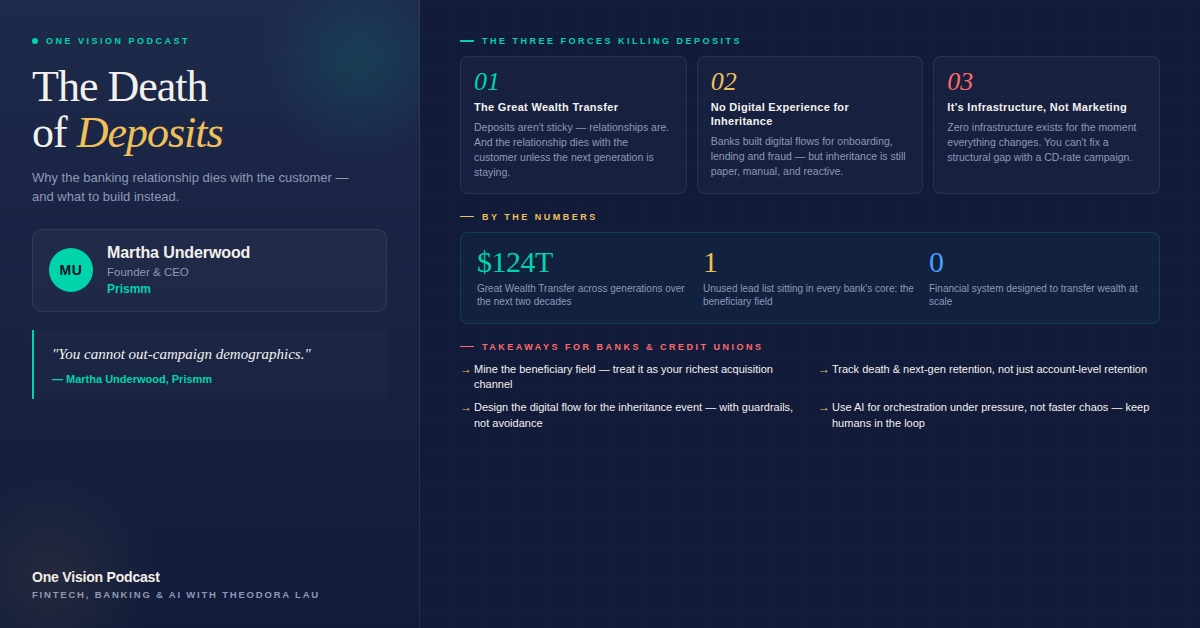

A few weeks ago, Martha Underwood, Founder and CEO of Prismm, and author of the newly released The Death of Deposits, joined us on the One Vision Podcast.

Here are three key takeaways from our conversation:

[1] Banks are in a "retention illusion".

Most institutions report strong retention numbers, because they are not tracking deaths or the retention of the next generation. Meanwhile, we are in the middle of the largest generational wealth transfer in history, and the relationship — not the deposit — is what makes money sticky. When the original account holder passes away, the relationship dies with them, unless the institution has already retained the beneficiary. But most haven't. And as Martha put it: "You cannot out-campaign demographics."

[2] The beneficiary field is the richest unused lead list in banking.

Sitting in every bank's core system is a field called "beneficiary". It contains a pre-qualified next-generation customer the institution will eventually need to serve ... for lending, for mortgages, and for all the grown-up stuff that fintechs can't easily replicate. According to Martha, this should be treated as an acquisition channel. And the institutions that build the relationship before the inheritance event are the ones that keep it after.

[3] AI's job is to bring control clarity to a moment of chaos.

When someone passes away, the typical bank process takes weeks just to give a beneficiary access to the inheritance. Automating the chaos doesn't remove the chaos. It just makes it faster chaos. The role of AI is quiet orchestration in the background: organizing accounts, mapping beneficiaries, flagging inconsistencies, and surfacing next steps to the human banker.

📚 The Death of Deposits is out now.

“Everyone thinks banks have all the answers when someone dies — because they should.”

If you missed our conversation, give the full episode a listen ... wherever you listen to podcasts.

Episode Transcript

1

00:00:04.850 --> 00:00:12.770

Hello everyone, welcome to a brand new episode of one vision the fintech fuse. This is Theo your host for today's episode

2

00:00:12.770 --> 00:00:15.970

Joining us on the show today is

3

00:00:16.710 --> 00:00:24.290

Martha Underwood founder of prison and the newly minted author of the death of deposits

4

00:00:24.290 --> 00:00:25.930

Welcome to the show Martha

5

00:00:25.930 --> 00:00:30.930

Thank you, Theo. I mean, we've been trying to get together for forever. So I'm so happy

6

00:00:30.930 --> 00:00:37.030

Finally doing this for a while for a while. It's the curse of our circle

7

00:00:37.030 --> 00:00:43.670

I feel like we're either really busy or we have time and then you make plans and then we just get busy

8

00:00:43.670 --> 00:00:47.010

But I am so glad that at least you know

9

00:00:47.010 --> 00:00:52.430

Cafe have brought us together and we were finally able to meet face-to-face. That was awesome

10

00:00:52.430 --> 00:00:54.490

and we'll get right into

11

00:00:54.490 --> 00:01:00.910

Cafe too, but this Christian and team are doing a great thing and you know, I I love them to pieces

12

00:01:00.930 --> 00:01:06.770

So before we get started about other people, let's talk about you

13

00:01:06.770 --> 00:01:09.770

So you had an interesting career

14

00:01:09.770 --> 00:01:14.210

You've been an IBM. You've been at BBB a

15

00:01:14.210 --> 00:01:15.850

compass and

16

00:01:15.850 --> 00:01:18.100

You're a founder. You're an author

17

00:01:19.030 --> 00:01:26.150

That's a lot of things on there. Tell us your story moving from big tech to inside of big banks tech

18

00:01:26.150 --> 00:01:29.890

Organization to now what's going on Martha?

19

00:01:30.810 --> 00:01:32.390

Yeah, so I

20

00:01:32.390 --> 00:01:40.450

It's interesting how my career just kind of ebbed and flowed right? So starting out of college at IBM

21

00:01:41.130 --> 00:01:46.190

What I learned and I always say growing up in IBM was the best thing because they make you kind of ambidextrous

22

00:01:46.190 --> 00:01:52.010

They put you in all of these seats, but I learned how to build at scale at IBM, right?

23

00:01:52.050 --> 00:01:59.810

You're designing for millions of users like there's complex workflows. There's regulated environment. So everything is about performance

24

00:02:00.390 --> 00:02:01.970

Everything is about reliability

25

00:02:01.970 --> 00:02:04.010

Everything is about precision

26

00:02:04.930 --> 00:02:06.820

and so then taking that

27

00:02:08.030 --> 00:02:14.780

Into banking and there's a lot in between there worked in Silicon Valley. I worked in data analytics did some stuff there

28

00:02:15.770 --> 00:02:18.230

but then landing at

29

00:02:19.130 --> 00:02:19.670

BBVA

30

00:02:20.210 --> 00:02:23.890

And really getting to see the back end of like banking systems

31

00:02:23.890 --> 00:02:27.770

I leaned on my IBM training because they they train you to look for

32

00:02:27.770 --> 00:02:35.290

Intersections and everything and one of the things that I saw is there is an unspoken

33

00:02:36.430 --> 00:02:43.330

Assumption baked into almost every system right and that assumption is that the user is always going to be there

34

00:02:43.330 --> 00:02:48.280

Like every flow starts with them. The processes depend on them

35

00:02:48.510 --> 00:02:53.380

like the outcomes depend on the presence and so

36

00:02:54.180 --> 00:03:00.160

Going to the bank and being a part of you know transformation and and

37

00:03:00.160 --> 00:03:01.140

digital

38

00:03:01.780 --> 00:03:06.040

Projects to bring, you know digital front doors to some of the old legacy systems

39

00:03:06.040 --> 00:03:11.320

That's when you really start to see where there might be some gaps, especially with what I do today

40

00:03:12.220 --> 00:03:17.720

But you're not just building software. You're building around people's lives, especially when you're talking about money

41

00:03:18.780 --> 00:03:20.460

and so that's

42

00:03:20.460 --> 00:03:28.300

Kind of how my mind worked around just looking at the systems and I think again, I think IBM for

43

00:03:29.040 --> 00:03:36.260

Being such trailblazers and how they trained us and how they conditioned us to think about solving and building

44

00:03:37.020 --> 00:03:41.380

For for users and at scale and I brought that over to BBVA with me

45

00:03:42.740 --> 00:03:46.400

And then next thing, you know, you have your own company

46

00:03:46.400 --> 00:03:52.500

Next thing, you know, I have prism and and you know prism was born out of personal need

47

00:03:53.220 --> 00:03:57.640

And professional experience, right? So, you know, I tell the story all the time about my dad

48

00:03:57.640 --> 00:04:01.060

And I also talk about prism was born out of love for my mom and dad

49

00:04:01.060 --> 00:04:06.840

Um, because when my dad had an accident in 2017 where he fell off the roof and went unconscious

50

00:04:08.040 --> 00:04:13.660

Um, my mom took him to the hospital and she was just frantic and they were peppering her with all types of questions

51

00:04:13.660 --> 00:04:15.340

Like how are you going to pay and all the things?

52

00:04:15.340 --> 00:04:21.100

And traditional family my mom and dad been married 64 years. Theo can't believe that I

53

00:04:21.100 --> 00:04:25.200

I don't know how they did it but or do it but it's awesome

54

00:04:25.960 --> 00:04:29.800

Um, but he's taking care of everything and so at that moment

55

00:04:29.800 --> 00:04:32.620

She calls, you know me and my sister and it's like hey

56

00:04:32.620 --> 00:04:38.080

Has your dad ever talked to you about where the money is and all the things and we're like no he hasn't

57

00:04:38.080 --> 00:04:39.200

and so

58

00:04:39.200 --> 00:04:41.400

we just knew of

59

00:04:41.400 --> 00:04:47.740

His financial advisor named gear mo who was this person he referenced every now and again and

60

00:04:48.660 --> 00:04:50.900

We're like in 30 years. We had never met him

61

00:04:50.900 --> 00:04:55.800

And so that was a wake-up call for us and thank god he ended up being okay

62

00:04:55.800 --> 00:04:59.220

And as soon as he was I was like we need to make sure

63

00:04:59.920 --> 00:05:03.320

That we know where your assets are because you have a lot

64

00:05:03.320 --> 00:05:06.860

So that if something happens to you mom is taking care of it, right?

65

00:05:07.340 --> 00:05:09.460

And so that was personal to me

66

00:05:10.020 --> 00:05:10.500

then

67

00:05:11.060 --> 00:05:12.900

Take that in 2020

68

00:05:12.900 --> 00:05:16.580

When covet hits and you have several people die

69

00:05:16.580 --> 00:05:17.400

unexpectedly

70

00:05:18.760 --> 00:05:22.200

And branch leader branch operations was under my leadership

71

00:05:22.900 --> 00:05:27.280

Um some of the the software and so we would see people come in

72

00:05:27.280 --> 00:05:32.000

After their loved one unexpectedly died of covet and looking for assets

73

00:05:32.000 --> 00:05:39.020

And i'm just kind of like, okay looking through our process and again it went back to all right. The user is always there

74

00:05:39.020 --> 00:05:44.220

What happens when the user is not there the system doesn't know what to do

75

00:05:44.780 --> 00:05:50.960

And that's when I witnessed how counts got frozen frozen, you know the family scramble

76

00:05:50.960 --> 00:05:57.660

And we were trying to put pieces together manually, you know at the bank and the money just sits there

77

00:05:57.660 --> 00:06:01.940

Not because we didn't care the banks didn't care. We didn't have processes didn't care

78

00:06:01.940 --> 00:06:05.320

But because the infrastructure was never designed for that moment

79

00:06:05.320 --> 00:06:09.670

And that's when that eureka hit me that this is not just a

80

00:06:11.000 --> 00:06:15.240

A human organization problem or a family organization problem

81

00:06:15.240 --> 00:06:17.440

you know, it's a

82

00:06:17.440 --> 00:06:23.520

Infrastructure problem because we've built all of these systems for onboarding for payments for fraud

83

00:06:23.520 --> 00:06:26.160

but nothing really for when

84

00:06:26.160 --> 00:06:28.260

everything actually changes

85

00:06:28.920 --> 00:06:32.920

And it's not an edge case. We know what's going to happen. It's a certainty

86

00:06:32.920 --> 00:06:35.400

But we created or we

87

00:06:36.300 --> 00:06:37.600

We treat it as an exception

88

00:06:38.360 --> 00:06:41.980

And and I think that's where I saw the opportunity

89

00:06:42.520 --> 00:06:44.820

And that's where that shift happened for me

90

00:06:45.420 --> 00:06:49.780

And I started seeing this more as an infrastructure gap. And so

91

00:06:49.780 --> 00:06:54.800

I said, well we can fix this, you know, we are smart. We're in it. I know what I

92

00:06:55.440 --> 00:06:58.980

Wanted to have when I experienced that moment with my dad

93

00:06:58.980 --> 00:07:03.420

And then I also know the professional experience I have being at the bank

94

00:07:04.100 --> 00:07:10.280

So we said, um, let's build it and so prism was was born and brought to market

95

00:07:11.120 --> 00:07:11.800

Wow

96

00:07:11.800 --> 00:07:14.900

I I love that story and so much of

97

00:07:15.320 --> 00:07:18.260

what you said resonates because um

98

00:07:19.000 --> 00:07:19.600

about

99

00:07:19.600 --> 00:07:25.540

Almost a decade ago that that was an area of focus. I was honed in on fintech is

100

00:07:25.540 --> 00:07:33.250

How do we serve older adults and their family members better right and one big key thing that came about is

101

00:07:33.660 --> 00:07:38.980

What happens at that transition moment to your point very often, you know

102

00:07:38.980 --> 00:07:41.710

you have head of the household the rest of the

103

00:07:42.000 --> 00:07:42.640

people

104

00:07:42.640 --> 00:07:49.980

aren't that familiar with you know, who has been helping to manage to finances right or

105

00:07:49.980 --> 00:07:55.460

You know, we have everything in a box actually I do i'll be the first one raise my hand

106

00:07:55.460 --> 00:07:59.340

I have all my papers and in a in a box

107

00:08:00.340 --> 00:08:00.940

um

108

00:08:00.940 --> 00:08:03.340

And now they're in folders

109

00:08:03.900 --> 00:08:04.520

Yeah

110

00:08:05.180 --> 00:08:07.060

Right. It's we don't

111

00:08:07.060 --> 00:08:12.000

As much as we are always busy running around doing everything and everything is digital, right?

112

00:08:12.200 --> 00:08:13.960

Look at look at around us

113

00:08:13.960 --> 00:08:17.260

the most important aspects of our lives

114

00:08:17.260 --> 00:08:21.040

Has always been so analog is relationship

115

00:08:21.700 --> 00:08:29.500

With people that we haven't really introduced to the rest of our family is relationship with our banks, which are all in papers

116

00:08:29.500 --> 00:08:33.820

um, and the thing you would appreciate this my uh

117

00:08:33.820 --> 00:08:38.159

Safety deposit box last year, which I finally closed after 30 something years

118

00:08:39.080 --> 00:08:45.080

They couldn't find my account at the bank branch when they were trying to close it

119

00:08:45.880 --> 00:08:46.440

um

120

00:08:46.440 --> 00:08:49.400

We had to go to a metal tin box

121

00:08:49.400 --> 00:08:54.700

With a little index card that they found my name and they're like, oh we found you

122

00:08:54.700 --> 00:08:58.920

This was after like trying to to find me in the system for more than 20 minutes

123

00:08:58.920 --> 00:09:00.880

so everything

124

00:09:00.880 --> 00:09:08.120

It's almost like why do we not design for it to your point, right? We know this was going to happen

125

00:09:08.120 --> 00:09:11.820

But yet we spent so much time looking at

126

00:09:12.500 --> 00:09:14.720

As you say onboarding

127

00:09:15.080 --> 00:09:16.460

fraud prevention

128

00:09:16.460 --> 00:09:20.840

Looking at accumulation rather than preparing for

129

00:09:20.840 --> 00:09:23.280

Decumulation and what happens after

130

00:09:23.880 --> 00:09:29.060

So this is very timely and I can't wait to dig into your book. I'm going to bring it

131

00:09:29.400 --> 00:09:33.580

On my trip this afternoon. So I will come back and tell stories

132

00:09:33.580 --> 00:09:39.180

So this is a good segue, right? Your new book the death of deposits

133

00:09:39.180 --> 00:09:44.560

Tell me more about the book and the key messages you want the readers to walk away with

134

00:09:45.080 --> 00:09:45.580

well

135

00:09:46.200 --> 00:09:49.750

the the key thing is it really is

136

00:09:50.980 --> 00:09:51.800

um

137

00:09:51.800 --> 00:09:59.630

A message to the community banks because the community banks are the ones that have deep relationships with

138

00:10:00.360 --> 00:10:03.840

The um, their consumers and with their customers, right?

139

00:10:04.580 --> 00:10:05.400

and

140

00:10:05.400 --> 00:10:07.630

it's not that um

141

00:10:08.460 --> 00:10:13.720

Deposits are dying or moving because people don't need banks. They need banks, right?

142

00:10:14.440 --> 00:10:16.660

They're dying or

143

00:10:16.660 --> 00:10:24.000

Decreasing at the banks that they we trust so much because the conditions that kept them there no longer really exist

144

00:10:24.000 --> 00:10:27.820

Right. So one of the things that I break down the three big things that

145

00:10:27.820 --> 00:10:30.500

If I were to summarize it

146

00:10:30.500 --> 00:10:34.660

I'd say is one we're in the largest wealth transfer in history, right?

147

00:10:34.740 --> 00:10:39.120

We all we keep talking about that and the deposits are no longer sticky, right?

148

00:10:39.240 --> 00:10:43.240

Because you got all of the fintechs there like the relationships are sticky

149

00:10:43.960 --> 00:10:46.140

That's the key and the relationships

150

00:10:47.520 --> 00:10:49.760

dies with the customer unless

151

00:10:50.520 --> 00:10:54.300

The bank has captured the next generation before the inheritance event

152

00:10:54.300 --> 00:10:59.900

I always talk about how the banks have this rich lead list and they're sitting in their cores

153

00:11:00.750 --> 00:11:01.720

in that

154

00:11:01.720 --> 00:11:03.480

Text field called beneficiary

155

00:11:03.480 --> 00:11:09.020

But they're not doing anything with it and and that's one of the things we do with prism is we surface that because

156

00:11:09.020 --> 00:11:10.780

You need to start building that relationship

157

00:11:10.780 --> 00:11:16.440

Before the inheritance event happens, um, the second big thing is that

158

00:11:17.860 --> 00:11:21.260

Customers now expect a digital experience, right?

159

00:11:21.720 --> 00:11:25.580

There's a digital experience with almost everything in the bank. Like we talked about lending

160

00:11:25.580 --> 00:11:29.860

You know fraud on the back end like there are automatic checks and things

161

00:11:30.560 --> 00:11:31.080

but

162

00:11:31.080 --> 00:11:35.180

There isn't one for this. This is the one that still is very manual

163

00:11:35.180 --> 00:11:39.560

like you talked about they had to go find you on the index card and I was laughing because

164

00:11:39.560 --> 00:11:41.520

I you believe that right?

165

00:11:41.780 --> 00:11:43.700

I can see that happening, right?

166

00:11:44.460 --> 00:11:47.960

um, and so and and I understand that

167

00:11:47.960 --> 00:11:49.620

With this, you know

168

00:11:49.620 --> 00:11:56.660

The fraud concerns are real because there are bad actors out there that can come in with falsified documents trying to get grandmas

169

00:11:56.660 --> 00:11:58.280

You know million dollars, right?

170

00:11:59.060 --> 00:12:05.760

But the answer to that is to really just build the guardrails within the experience like we do with everything else

171

00:12:05.760 --> 00:12:08.280

Right not to avoid the experience

172

00:12:08.920 --> 00:12:17.060

Altogether, right? We need to figure out what does that digital experience look like when an inheritance event happens?

173

00:12:17.600 --> 00:12:20.120

For the next generation. So that's the other

174

00:12:20.120 --> 00:12:23.240

Thing that's the second thing and then i'd say

175

00:12:23.240 --> 00:12:26.280

You know the third thing. Um

176

00:12:26.280 --> 00:12:27.980

Is this is an infrastructure problem?

177

00:12:28.460 --> 00:12:33.280

It's not a marketing problem, right? Because you cannot out campaign demographics

178

00:12:34.040 --> 00:12:34.600

right

179

00:12:35.160 --> 00:12:39.300

Oh, I was just because someone was just like we'll just run a campaign

180

00:12:39.920 --> 00:12:45.880

And try to get you know run cds like a new cd that with this great raid and all and i'm like

181

00:12:45.880 --> 00:12:48.740

You can't out campaign demographics, right?

182

00:12:49.060 --> 00:12:52.000

And right now we have zero infrastructure for that moment

183

00:12:52.780 --> 00:12:53.900

and so

184

00:12:53.900 --> 00:12:57.560

The core message overall is really simple

185

00:12:58.280 --> 00:12:59.740

If you don't design

186

00:12:59.740 --> 00:13:02.460

For the transfer you're going to lose the relationship

187

00:13:03.900 --> 00:13:04.460

Okay

188

00:13:04.460 --> 00:13:06.520

I can't agree more to sign for the transfer

189

00:13:06.520 --> 00:13:11.420

The other joke I used to make is that you know, we keep talking about the wealth transfer

190

00:13:11.420 --> 00:13:15.020

But if you don't protect the assets of those people

191

00:13:15.600 --> 00:13:18.160

There will be no assets left to transfer

192

00:13:19.080 --> 00:13:21.500

So, you know

193

00:13:21.500 --> 00:13:26.740

We can all adjust and you know jeans and you know, try to attract the millennial

194

00:13:26.740 --> 00:13:29.080

This was back 10 years ago or the gen z

195

00:13:29.080 --> 00:13:33.280

Now but he got to take care of the basics first

196

00:13:34.440 --> 00:13:41.620

It seems it seems simple. Um, I love what you were saying. You cannot it's not a marketing campaign problem. Definitely. It's not

197

00:13:42.360 --> 00:13:51.160

In your view, you know when we talk about the the the title of the book caught me it was it was interesting. It's it's um

198

00:13:51.160 --> 00:13:56.560

It's almost provocative and it stands out because it's you're trying to get people's attention

199

00:13:57.940 --> 00:13:59.060

Right that

200

00:13:59.760 --> 00:14:03.940

That was the intention brilliantly done it caught my attention

201

00:14:03.940 --> 00:14:10.140

Um, but when we think about you know dying, right we think about the physical. Um

202

00:14:10.140 --> 00:14:11.420

Um passing away

203

00:14:11.420 --> 00:14:17.720

Um, and as you say it's not the deposit is not dying because it the money is there is just at the

204

00:14:17.720 --> 00:14:21.200

Relationship that you had with the people is is gone

205

00:14:22.640 --> 00:14:23.200

um

206

00:14:23.200 --> 00:14:24.860

Why do then

207

00:14:25.540 --> 00:14:31.860

Why do the bankers still inherently assume that people is just going to keep going along with it

208

00:14:33.180 --> 00:14:39.460

Because it's easier out it's it's easier it's easier. Um, and

209

00:14:39.460 --> 00:14:41.280

This is a

210

00:14:41.280 --> 00:14:44.560

This is a heavy lift for them and it's a mindset shift

211

00:14:45.440 --> 00:14:50.020

Because in banking they have accepted death as natural attrition

212

00:14:50.640 --> 00:14:55.100

And so you'll enjoy the the section where I talk about the retention illusion

213

00:14:55.740 --> 00:15:02.600

Where when you talk to you know bankers they're like, oh we have great retention rates. That's because they're not tracking

214

00:15:03.600 --> 00:15:04.720

the um

215

00:15:04.720 --> 00:15:09.000

Deaths rates right and retention of the next generation, right?

216

00:15:09.260 --> 00:15:16.460

And so what's dying for me is like what you said is that they have this assumption, but that's dying right the assumption layer

217

00:15:17.420 --> 00:15:20.220

That the relationship transfers with money

218

00:15:21.020 --> 00:15:23.700

That the next generation is going to stay by default

219

00:15:24.220 --> 00:15:27.260

And that loyalty survives life events

220

00:15:27.880 --> 00:15:29.260

None of those are true

221

00:15:29.800 --> 00:15:30.720

Not anymore

222

00:15:30.720 --> 00:15:39.100

Right because when you really look at it the next generation did not open the account with you their parents did or their grandparents did

223

00:15:39.100 --> 00:15:40.520

They don't know the banker

224

00:15:41.080 --> 00:15:46.040

They have zero emotional ties to it, right? Because again

225

00:15:46.460 --> 00:15:49.960

in this new world order of digital convenience

226

00:15:50.870 --> 00:15:53.030

They already have apps that they trust

227

00:15:53.560 --> 00:15:56.270

Um platforms that they're already using and so

228

00:15:56.680 --> 00:16:03.560

If you don't have something that can provide them speed and clarity, especially during this time when they are grieving

229

00:16:03.560 --> 00:16:05.460

Or they're emotional

230

00:16:06.300 --> 00:16:06.960

then

231

00:16:07.580 --> 00:16:09.320

When the time comes

232

00:16:09.320 --> 00:16:14.080

For you to be their bank, you know, they're not going to choose you

233

00:16:14.080 --> 00:16:20.360

And also, I think the next generation looks at money a little different they don't necessarily see a bank

234

00:16:21.340 --> 00:16:25.400

Um, because when you ask them about banks like when I asked my son about a bank

235

00:16:25.400 --> 00:16:29.080

He's like, oh then more cash happening. I'm like they're not banks, right?

236

00:16:29.540 --> 00:16:33.280

Yeah, my kids call apple the bank right they call and so

237

00:16:33.280 --> 00:16:35.680

But because they see money in motion

238

00:16:36.560 --> 00:16:38.800

Right that that's how they look at it

239

00:16:39.440 --> 00:16:44.200

As they get older they're going to realize that they're going to need a relationship with the bank

240

00:16:44.200 --> 00:16:48.460

For lending for mortgages for all the grown-up stuff, right?

241

00:16:49.000 --> 00:16:50.320

and so

242

00:16:50.320 --> 00:16:54.500

The the thing is that I think that the banker should be thinking about

243

00:16:54.500 --> 00:16:58.820

Is not have that assumption that that money will will automatically stay

244

00:16:59.600 --> 00:17:00.000

right

245

00:17:00.680 --> 00:17:02.720

It's it's how do I?

246

00:17:03.460 --> 00:17:11.599

Ensure that i'm connected to that next generation so that they believe that this money should continue to live here

247

00:17:12.520 --> 00:17:15.960

And you cannot do that just by pretending to be hip

248

00:17:16.560 --> 00:17:18.480

Correct. That doesn't work

249

00:17:19.400 --> 00:17:24.000

No, it doesn't work right and and so

250

00:17:24.000 --> 00:17:27.619

The thing is the default inheritance of the relationship

251

00:17:29.280 --> 00:17:32.540

Because they think that they're going to inherit the relationship by default

252

00:17:32.720 --> 00:17:36.980

That has died that is that is no longer the case. You have too many other tools

253

00:17:36.980 --> 00:17:39.760

That the fintechs have optimized for

254

00:17:39.760 --> 00:17:42.180

To make it easy to move money there

255

00:17:42.180 --> 00:17:49.720

Even though they don't have all of the the robust products or even the governance and compliance and guardrails that

256

00:17:49.720 --> 00:17:51.540

the institutional banks have

257

00:17:52.080 --> 00:17:56.760

The younger generation just does not see it that way. And so this is a great opportunity

258

00:17:57.580 --> 00:17:58.100

for

259

00:17:58.100 --> 00:18:01.660

the community banks and banks at large and credit unions

260

00:18:02.300 --> 00:18:04.720

To be able to again design

261

00:18:05.300 --> 00:18:07.880

For the relate to capture the relationship

262

00:18:07.880 --> 00:18:10.660

Of the beneficiaries because that will be their

263

00:18:11.680 --> 00:18:14.040

That that's their secret weapon

264

00:18:14.640 --> 00:18:19.220

Because I know that my son had an issue with cash app and he's like mom. Can you call them?

265

00:18:19.800 --> 00:18:26.720

Like there's no calling. Yeah, there's no calling. There's no calling right? And so that's the thing but I can call the bank

266

00:18:26.720 --> 00:18:32.800

Yes, right at least get someone or I can at least go into a branch and talk to someone so that that human

267

00:18:33.860 --> 00:18:34.420

interaction

268

00:18:35.460 --> 00:18:42.260

um, especially at the time of inheritance and I know of you before the inheritance event

269

00:18:42.880 --> 00:18:47.380

You're looking at the emotional connection that you're going to build with that

270

00:18:47.720 --> 00:18:54.320

With that beneficiary to your institution and to that money that lives there and the banks that do it first

271

00:18:54.320 --> 00:18:59.180

They went when they the ones that see this as the infrastructure that it should be

272

00:18:59.180 --> 00:19:01.100

And build it now

273

00:19:01.100 --> 00:19:02.720

through prism, of course

274

00:19:03.660 --> 00:19:04.180

then

275

00:19:04.800 --> 00:19:10.080

They will they really will end and and if they're starting to think about that and that's what I tried to capture

276

00:19:10.080 --> 00:19:14.840

In the book I didn't I wanted to be able to speak the banker's language

277

00:19:14.840 --> 00:19:21.920

Through storytelling as well as through processes because I also looked at you know did research in

278

00:19:22.720 --> 00:19:25.780

How long does it really take? What are all of the steps?

279

00:19:26.500 --> 00:19:31.060

Right, and as you go through it, you'll see that in some cases there's 21 steps

280

00:19:31.840 --> 00:19:38.740

just to get access to the cash in the bank account that I am a beneficiary of

281

00:19:39.440 --> 00:19:47.640

And how many people that you might have to touch or retell the story or retell your situation or resubmit documents?

282

00:19:48.640 --> 00:19:54.680

Because it's so siloed and they're not taught the systems aren't talking to each other internally and so that's

283

00:19:55.740 --> 00:20:02.960

Really what I want the bankers to understand and to see that this is a mindset shift and shift and they can really

284

00:20:02.960 --> 00:20:06.940

Take advantage of this and and safeguard the money

285

00:20:06.940 --> 00:20:09.500

That you know the kids will inherit

286

00:20:10.660 --> 00:20:14.140

Because they're going to need guidance. They're going to need to understand

287

00:20:14.760 --> 00:20:16.080

You know the basics

288

00:20:16.080 --> 00:20:21.440

Basic principles of money not because they don't see it because it's digital

289

00:20:22.000 --> 00:20:24.280

They don't have sometimes the same value

290

00:20:24.280 --> 00:20:30.600

That we have had and the banks understand right because again, like they said they see they just see money in motion

291

00:20:30.600 --> 00:20:33.780

They just see it's here one day and then it's there the next day

292

00:20:34.960 --> 00:20:36.080

um, so

293

00:20:36.080 --> 00:20:38.540

And that's like even assuming

294

00:20:39.120 --> 00:20:44.500

To your point that's money that you already have and should have access to

295

00:20:44.500 --> 00:20:49.460

We haven't even touched on all of the months before that which is you know, if you don't have

296

00:20:50.120 --> 00:20:54.300

A will drawn up and you don't have any of those those are you know

297

00:20:54.300 --> 00:20:57.220

think about the emotional drain

298

00:20:58.340 --> 00:21:04.940

Of people by the time they get through all that mess and then to the bank. They're already like exhausted

299

00:21:08.300 --> 00:21:13.720

Okay, all right shift gears a little bit, okay, um

300

00:21:13.720 --> 00:21:15.820

You've started prism. Yep

301

00:21:15.820 --> 00:21:22.020

Writing a book you've gone through the cafe as a accelerator two questions. Sure

302

00:21:22.020 --> 00:21:23.120

one is

303

00:21:23.120 --> 00:21:25.220

How has the reception been?

304

00:21:25.560 --> 00:21:29.420

You know of of prism in the wider banking

305

00:21:29.940 --> 00:21:32.100

community and then

306

00:21:32.100 --> 00:21:33.180

also

307

00:21:33.980 --> 00:21:38.620

Why did you choose cafe and how is that different than you know, traditional yc playbooks?

308

00:21:38.620 --> 00:21:41.700

That's always like something people ask great, you know if i'm a startup

309

00:21:41.700 --> 00:21:47.160

Um, I wanted to reach out to a broader network. Who do I go to and why?

310

00:21:48.560 --> 00:21:55.100

So first question is how is prism being received at banks and it's being well received they are

311

00:21:56.160 --> 00:22:01.220

Catching up like we've been at this for five years and at first it was kind of like, yeah, I don't know right

312

00:22:01.880 --> 00:22:02.360

but

313

00:22:02.360 --> 00:22:05.880

I think there are a lot of market signals

314

00:22:06.580 --> 00:22:09.340

That is telling them that wow

315

00:22:09.340 --> 00:22:14.720

This is something that we should be focused on because we already have the assets in house

316

00:22:15.240 --> 00:22:18.180

One of the things that we've been doing is showing them the data

317

00:22:18.180 --> 00:22:24.960

Is looking at the demographics of their deposit holders. How old are they what percentage?

318

00:22:25.900 --> 00:22:27.740

of dollars that they have and then

319

00:22:28.260 --> 00:22:29.960

correlating that to

320

00:22:29.960 --> 00:22:34.000

Account openings new account openings, right? It's not it's not growing fast enough

321

00:22:34.740 --> 00:22:37.060

And so why

322

00:22:37.060 --> 00:22:43.040

Try to spend money to get net new customers when again you have this rich lead list

323

00:22:43.040 --> 00:22:47.560

In that field called beneficiaries sitting in your cores that you're not engaging

324

00:22:48.500 --> 00:22:50.920

And when I start to show them the numbers

325

00:22:51.760 --> 00:22:52.360

of

326

00:22:52.360 --> 00:22:56.500

What the cost of customer acquisition is?

327

00:22:57.120 --> 00:23:01.940

What the cost of broker deposit is as their deposits start to

328

00:23:01.940 --> 00:23:04.140

To dwindle right?

329

00:23:04.480 --> 00:23:09.220

Just showing them just how much attrition is happening as it relates to death

330

00:23:09.220 --> 00:23:13.640

Versus how many new accounts are coming in they're really starting to

331

00:23:14.240 --> 00:23:19.600

See how this is a benefit to them and it's being well received

332

00:23:19.600 --> 00:23:24.020

and so the conversation that i'm having and the one of the

333

00:23:24.020 --> 00:23:31.200

Phrases that I coined is we need to look at inheritance infrastructure because we've never had it because we never had to have it

334

00:23:31.200 --> 00:23:38.520

Right. Um, and so it's really being well received and and I have to thank cafe for that actually, too

335

00:23:39.120 --> 00:23:41.060

um because

336

00:23:41.060 --> 00:23:43.000

I chose them

337

00:23:43.600 --> 00:23:45.680

Because of the access they provided

338

00:23:46.740 --> 00:23:48.580

It it wasn't

339

00:23:49.440 --> 00:23:52.300

Just all programming and you're just sitting in a room

340

00:23:52.300 --> 00:23:55.860

It was you get access to get membership with the aba

341

00:23:55.860 --> 00:24:02.120

You get access to get membership with you know, the american fintech council and aba is the american bankers association

342

00:24:02.660 --> 00:24:04.990

right, and so what

343

00:24:05.440 --> 00:24:10.580

Cafe, I would say teaches teaches you that maybe a yc doesn't

344

00:24:11.240 --> 00:24:13.760

Is how to move with the system?

345

00:24:14.360 --> 00:24:16.100

Or within the system

346

00:24:16.650 --> 00:24:19.260

Like yc they want you to move fast

347

00:24:19.780 --> 00:24:22.900

They're looking at products that can sell fast and move fast, right?

348

00:24:22.900 --> 00:24:28.020

And in fintech, especially with banking that distinction really matters because banks

349

00:24:28.740 --> 00:24:30.640

They operate off a trust

350

00:24:31.620 --> 00:24:38.400

Like you and and i've been building this for a while and i'm like i'm i'm one of y'all i'm a banker like y'all on the tech side

351

00:24:39.040 --> 00:24:43.400

But they are still like, uh, we still need to trust you, right?

352

00:24:43.720 --> 00:24:50.440

And so what what cafe unlocked for me was that access to the regulators to the banks

353

00:24:50.440 --> 00:24:52.800

to real distribution channels

354

00:24:53.500 --> 00:25:00.000

And then credibility inside of the the the ecosystem because i'm able to have those one-on-one conversations

355

00:25:00.000 --> 00:25:06.420

I'm able to talk to their challenges and show that I truly understand it not just from a consumer perspective

356

00:25:06.420 --> 00:25:11.180

But being on the inside having to work with the business units as well as on the tech side

357

00:25:11.180 --> 00:25:13.240

And what challenges you may have?

358

00:25:13.660 --> 00:25:14.240

when

359

00:25:14.820 --> 00:25:21.560

You're looking at a new platform or even new infrastructure. What does that really take?

360

00:25:21.560 --> 00:25:26.740

And so if you're building like a consumer app, why see all day, right that works

361

00:25:26.740 --> 00:25:28.780

They're going to give you everything you need

362

00:25:28.780 --> 00:25:36.200

To be able to to build and deploy and scale right? But if you're building like a financial infrastructure

363

00:25:36.200 --> 00:25:42.030

Then you need proximity to those those institutions and that's what cafe really gave us

364

00:25:42.560 --> 00:25:44.720

and so that's um

365

00:25:44.720 --> 00:25:48.280

That's great. It exposed us to so many different opportunities

366

00:25:48.280 --> 00:25:52.580

Like we got the sscbi we got the edge grant the support there

367

00:25:52.580 --> 00:25:55.400

Um, and they're on the cutting edge, right?

368

00:25:56.080 --> 00:25:58.260

They they really are and so I

369

00:25:58.260 --> 00:25:59.020

I

370

00:25:59.020 --> 00:26:02.400

am so happy that I chose them because I was looking at

371

00:26:02.860 --> 00:26:05.640

What are the organizations or the?

372

00:26:06.440 --> 00:26:07.720

fintech specific

373

00:26:09.120 --> 00:26:12.460

Right accelerators that can give you access

374

00:26:12.460 --> 00:26:13.820

to customers

375

00:26:14.600 --> 00:26:21.960

And that's that's the benefit that cafe has so i'll always be a fan um christin and the team is they're amazing

376

00:26:22.680 --> 00:26:26.260

Um, and so yeah, I I think that's the differentiator

377

00:26:26.260 --> 00:26:31.680

I'm so happy to hear that and you were the first cohort like literally a second

378

00:26:31.680 --> 00:26:38.360

Okay, I was the second cohort and so um, it's yes amazing because now they're up to fifth, right?

379

00:26:38.400 --> 00:26:41.240

If I remember fourth or fifth i'm losing count

380

00:26:41.240 --> 00:26:48.500

I don't know. I think they're the six. I think it's the six cohort. So yeah, i'm like way behind. They're just moving

381

00:26:48.500 --> 00:26:54.140

um, and it's amazing and you know, finally I got the chance to see the um

382

00:26:54.140 --> 00:26:56.820

The the building and thoughts is nice

383

00:26:56.820 --> 00:27:01.100

It's gorgeous and I just I I love the mission as well

384

00:27:01.100 --> 00:27:05.800

You know to your point, you know, there are other accelerators depends on what you need

385

00:27:05.800 --> 00:27:10.900

But you know if you're building in this ecosystem you need access to the regulators

386

00:27:10.900 --> 00:27:16.400

You need access to distribution you need access to basically, you know, everyone that would touch

387

00:27:16.980 --> 00:27:23.400

And receive and give you guidance on what you're doing. And you know, that is the perfect spot plus they're mission driven

388

00:27:23.400 --> 00:27:30.180

You know, I i'm always a sucker for mission driven. Um, and you know, christin and ryan are amazing people. So

389

00:27:30.720 --> 00:27:33.500

And they brought us together. So i'm grateful for that

390

00:27:34.480 --> 00:27:40.720

Now, of course, I cannot let you go without asking you the buzzword of

391

00:27:40.900 --> 00:27:45.920

The year the decade. I don't know. I think next year is going to be something else. But for now it is ai

392

00:27:45.920 --> 00:27:47.520

Everyone is talking about ai

393

00:27:48.100 --> 00:27:54.660

Now in the first last 25 minutes or so we're talking about trust. We're talking about relationship

394

00:27:54.660 --> 00:28:00.300

We're talking about all those things that surround inheritance and wealth

395

00:28:00.960 --> 00:28:06.260

on the other side of the coin everyone's talking about ai and ai agents and you know data and

396

00:28:06.980 --> 00:28:08.500

How does that?

397

00:28:08.760 --> 00:28:10.560

How does that um

398

00:28:10.560 --> 00:28:16.340

Come together because data often when we think about is bits and bytes and cold and you know

399

00:28:16.340 --> 00:28:21.600

We're talking about inheritance and and those special moments. They're emotional is family

400

00:28:23.540 --> 00:28:28.460

How is is that something that ai can help and how does it help?

401

00:28:29.280 --> 00:28:36.720

Yeah, so we're you know, we're leveraging ai as well and where I see ai is in the background, right? It's quiet

402

00:28:36.720 --> 00:28:38.120

It's precise

403

00:28:38.120 --> 00:28:42.420

It's invisible like no one sees it just like infrastructure when it works. It just works

404

00:28:42.420 --> 00:28:46.780

The real role of ai really is just orchestration under pressure

405

00:28:48.320 --> 00:28:49.440

and so

406

00:28:49.440 --> 00:28:52.260

the thing is when um

407

00:28:53.760 --> 00:28:58.020

I'm just going to take a real example. I'm going to talk through like a real scenario here

408

00:28:58.020 --> 00:29:05.200

So when a customer passes away, right today that triggers chaos in the bank because it's it's all manual, right?

409

00:29:05.200 --> 00:29:09.560

The family don't know where everything is the bank gets, you know incomplete information

410

00:29:09.560 --> 00:29:13.240

They don't have all of the the files they need the accounts get frozen

411

00:29:13.240 --> 00:29:18.640

So people don't have access to the money, you know weeks of back and forth all of the things because it's manual

412

00:29:19.760 --> 00:29:20.240

so

413

00:29:20.240 --> 00:29:22.500

Imagine um at that same moment

414

00:29:23.680 --> 00:29:24.160

that

415

00:29:24.160 --> 00:29:26.720

With ai inside of prism you trigger the account

416

00:29:27.380 --> 00:29:33.420

ai already has all organized all of the accounts you've already put it in but it's organized those accounts the policies

417

00:29:33.420 --> 00:29:34.820

the documents

418

00:29:34.820 --> 00:29:38.480

You know mapped out the beneficiaries all of the permissions

419

00:29:38.480 --> 00:29:42.960

flagged all of the inconsistencies and then presents that up to the banker

420

00:29:44.400 --> 00:29:49.140

And says here are your next steps right because I still think that you need a human in a loop with this

421

00:29:49.140 --> 00:29:51.180

To verify those things, right?

422

00:29:51.880 --> 00:29:53.440

So then when the death is verified

423

00:29:53.440 --> 00:29:59.200

Then the the system shifts then now the accounts are ready to move money is ready to move the beneficiaries

424

00:29:59.200 --> 00:30:02.640

Other beneficiaries are notified that they get here's what they're going to get

425

00:30:02.640 --> 00:30:11.280

And then ai kind of guides them, right? It's meant to be a orchestration level to help organize and help you move things

426

00:30:12.000 --> 00:30:15.740

The other thing that I think that we need to be very careful with around

427

00:30:16.560 --> 00:30:20.300

Agents is access to the information and data the sensitive data, right?

428

00:30:20.680 --> 00:30:27.520

And making sure that the guardrails and the security is in place to secure the information that they will have right?

429

00:30:28.360 --> 00:30:30.500

So all of that makes

430

00:30:30.500 --> 00:30:34.520

Takes this very manual long process

431

00:30:34.520 --> 00:30:36.900

And synthesizes it down

432

00:30:36.900 --> 00:30:38.440

to hours

433

00:30:39.060 --> 00:30:41.440

right and now what you're doing is

434

00:30:42.220 --> 00:30:44.940

Using humans to verify and validate

435

00:30:45.620 --> 00:30:53.580

That that that is it it and it really just the ai really just prepares the transaction the transition. Um

436

00:30:53.580 --> 00:30:54.140

path

437

00:30:54.140 --> 00:30:55.140

right

438

00:30:55.140 --> 00:30:57.560

Because right now humans are doing that

439

00:30:57.560 --> 00:31:04.600

And then it'll flag any of the compliance issues or or they'll surface any of the issues before the money is moved

440

00:31:04.600 --> 00:31:10.760

So now you know, okay, I have an exception here that I need to do something. So instead of confusion you have

441

00:31:10.760 --> 00:31:13.940

Control clarity is what I like to call it, right?

442

00:31:16.480 --> 00:31:18.960

You don't have faster chaos

443

00:31:18.960 --> 00:31:22.680

Because I put more bodies against it you have

444

00:31:23.160 --> 00:31:25.940

Smart continuity and that's what the banks need

445

00:31:25.940 --> 00:31:32.720

They when you talk about an inheritance event, I call it a liquidity event when someone dies

446

00:31:33.440 --> 00:31:36.160

And if you add ai to it

447

00:31:36.640 --> 00:31:38.620

Bring some of the efficiencies

448

00:31:38.620 --> 00:31:41.320

That ai can bring to it

449

00:31:41.320 --> 00:31:44.840

You can bring that continuity to your process, right?

450

00:31:45.320 --> 00:31:47.340

um, and and I think that

451

00:31:47.340 --> 00:31:53.720

With the ai agents what the industry keeps asking is how do we automate more? How do we automate more?

452

00:31:53.720 --> 00:31:59.140

And I don't think that that's the right question, you know, I think the question is

453

00:31:59.140 --> 00:32:00.620

um

454

00:32:00.620 --> 00:32:02.400

How do we show up?

455

00:32:02.980 --> 00:32:04.640

with precision

456

00:32:05.640 --> 00:32:08.680

And clarity and the moments that matter most

457

00:32:09.480 --> 00:32:12.600

That's where ai really earns its stripes

458

00:32:13.400 --> 00:32:18.580

Right, and I think that that's where we we should be focused on

459

00:32:18.580 --> 00:32:21.860

Is looking at our systems and seeing

460

00:32:22.500 --> 00:32:24.500

Where can we make

461

00:32:25.220 --> 00:32:28.840

The process a lot more precise and easier for the consumer

462

00:32:29.520 --> 00:32:33.780

To be able to do things and in our case at death when you're emotional

463

00:32:34.340 --> 00:32:39.720

You're you are looking for speed because you need answers because you need to handle the business of death is what I call it

464

00:32:40.660 --> 00:32:44.540

um, and so you need to be able to validate all of those things like there's

465

00:32:45.100 --> 00:32:47.140

Several different things that need to be validated

466

00:32:47.140 --> 00:32:51.040

That ai can do pretty rapidly and I think that's where we should be focused

467

00:32:51.040 --> 00:32:55.460

And that's where you know, honestly where we're focused with prism and how we're leveraging ai

468

00:32:55.460 --> 00:33:00.340

And how we thought about architecting it into our process

469

00:33:01.620 --> 00:33:08.280

I like what you said, it's not just about automating. Um that that is precisely the wrong question

470

00:33:08.280 --> 00:33:09.800

Especially given the circumstance

471

00:33:09.800 --> 00:33:12.880

Um the use case that you're talking about

472

00:33:13.520 --> 00:33:14.100

um

473

00:33:14.680 --> 00:33:19.400

I love the human aspect you brought to it. I I'm a fan

474

00:33:19.960 --> 00:33:25.880

I'm just gonna come on sad. I'm fine. We gotta keep the humans in the loop, right because it's an emotional moment

475

00:33:26.440 --> 00:33:29.320

It is you can't just keep it all digital, right?

476

00:33:29.780 --> 00:33:33.160

You have to be able to have someone because ai doesn't

477

00:33:34.460 --> 00:33:39.500

Ai can't give empathy to the person standing in front of you that their mom just died

478

00:33:40.020 --> 00:33:42.620

And you know, they have teenage boys

479

00:33:43.220 --> 00:33:45.400

But they have to try to keep together

480

00:33:45.960 --> 00:33:47.960

Because they have so many other things to do

481

00:33:48.600 --> 00:33:53.880

Ai is there to help make that process easier. So me as the the banker that

482

00:33:54.440 --> 00:33:56.320

This person walked in

483

00:33:56.320 --> 00:33:58.600

Can just say hey, you know what? It's okay

484

00:33:59.240 --> 00:34:07.240

We have it we have the process ready. We understand what you need and hear the next steps because the reality is

485

00:34:07.880 --> 00:34:11.480

Everyone thinks that the bank has all the answers because they should

486

00:34:11.480 --> 00:34:12.960

when someone dies

487

00:34:14.080 --> 00:34:16.580

And that's not always the case

488

00:34:17.159 --> 00:34:21.540

And so I think again that's where ai can really earn the stripes and shine

489

00:34:21.540 --> 00:34:26.800

Is we just use it as a background optimizer and really just helps us

490

00:34:27.560 --> 00:34:30.179

be precise in how we

491

00:34:30.179 --> 00:34:32.460

We execute on

492

00:34:32.460 --> 00:34:34.920

Like I said the moments that matter

493

00:34:34.920 --> 00:34:39.780

Everyone thinks banks have all the answers everyone thinks banks have all the data

494

00:34:39.780 --> 00:34:45.360

But that doesn't mean that they can bring them together or rent provide you with what you need

495

00:34:46.000 --> 00:34:47.620

Before I let you go

496

00:34:47.620 --> 00:34:53.310

Martha, what is the one thing that you wish the industry would pay more attention to?

497

00:34:54.699 --> 00:34:55.639

What i'm doing

498

00:34:57.660 --> 00:35:04.300

Yes, everyone go follow martha but but in all seriousness, um, I I think you're absolutely right

499

00:35:05.180 --> 00:35:05.760

we

500

00:35:05.760 --> 00:35:08.920

May not always be paying attention to what matters

501

00:35:09.560 --> 00:35:15.240

Not just to the human side of things but understanding the human side of things will bring

502

00:35:16.120 --> 00:35:17.320

the operational

503

00:35:18.120 --> 00:35:20.420

Excellence that people are looking for

504

00:35:20.420 --> 00:35:26.720

We seem to be going for the for the answer in the wrong way all the time, right? Everyone wants more

505

00:35:27.440 --> 00:35:31.660

Deposits they want more customers. They want more businesses

506

00:35:32.520 --> 00:35:38.260

But we're going about not really the way that would seem the human way of doing it

507

00:35:38.260 --> 00:35:40.700

Yeah, because they are everyone's talking about acquisition

508

00:35:41.520 --> 00:35:43.140

How do we get more customers?

509

00:35:43.620 --> 00:35:51.140

Like you said more deposits and really they should just be asking how do we extend the relationship beyond the original account holder?

510

00:35:51.340 --> 00:35:56.360

How do you take care of the people you have right and their families? Yes

511

00:35:58.200 --> 00:36:00.300

It is very simple

512

00:36:00.300 --> 00:36:03.620

Um, so until we meet again martha

513

00:36:03.620 --> 00:36:07.280

Thank you so much for spending time with us and i'll put the

514

00:36:07.280 --> 00:36:09.680

The link of your book

515

00:36:10.240 --> 00:36:15.620

Uh from amazon, I believe it is now on the death of deposits on the show notes as well

516

00:36:15.620 --> 00:36:20.000

So thank you so much for joining us today on the show

517

00:36:20.560 --> 00:36:26.020

Thank you and for the rest of our listeners. Thank you so much for joining us for another episode of one vision

518

00:36:26.020 --> 00:36:27.200

Let's talk to you next week